It’s been awhile since my last blog post. Given the lapse of time this post will be number 7 in my top 10, Create Options. I have to admit, this one is near and dear to my heart.

I’ll start with what not to do, something I learned the hard way. In my 20s after I got my first real paycheck I sold by 1984 Olds Cutlass and bought a used Cadillac. It was time to move up in the world! The Olds needed a new muffler, otherwise it was in good shape. The Cadillac turned out to be a lemon. It needed an engine replacement, new suspension, and had electrical problems. In hindsight, spending $200 on a new muffler is what I should’ve done, but the Caddy was so cool looking that I was blinded by prestige. I went into debt to finance the Cadillac, got into more debt by needing to fix it, then I lost my patience and made the worst mistake I possible could’ve done: I traded it in on a new car. It was emotional decision that I was stuck paying off for the next 4 years.

Problems continued to compound because occurred circa 2000. I just lost my job in the dot com bubble. I still had those car payments, and I was way upside down in the new car. If I had not overspent on that damn Cadillac in the first place, things would’ve been great. I would have saved money and kept myself out of debt. I could have travelled or anything else, but I was stuck. The lesson learned is that I pigeon-holed myself financially. I made the assumption that my income was bulletproof.

We see this all the time with people buying too much house, fancy cars, or creating a lifestyle that isn’t sustainable long term if there is a speedbump in life. It’s how we go into a situation that determines whether that speedbump becomes a landmine or not. Losing your job and having savings to travel or facilitate a career change is a bump. Losing your job and being stuck with negative cash flow for the foreseeable future is much worse.

I view life as one big game of chance, much like cards. Just like in life, you can be dealt good or bad cards. In poker you can bluff a bad hand: those who live for the moment and live beyond their means. It works sometimes but eventually catches up to you. Instead, you could wait for the perfect hand and you might be stuck waiting for a while: those who save and save and let life pass them by. Or you can play a hand that is mediocre but may turn great if you get a good draw. Whether you play poker, gin, or cribbage you know the value of setting yourself up for a good draw card. Sometimes that costs some certainty but could payoff huge. So, in life how do we set up our “hand” to get a good draw? Here are a few ideas:

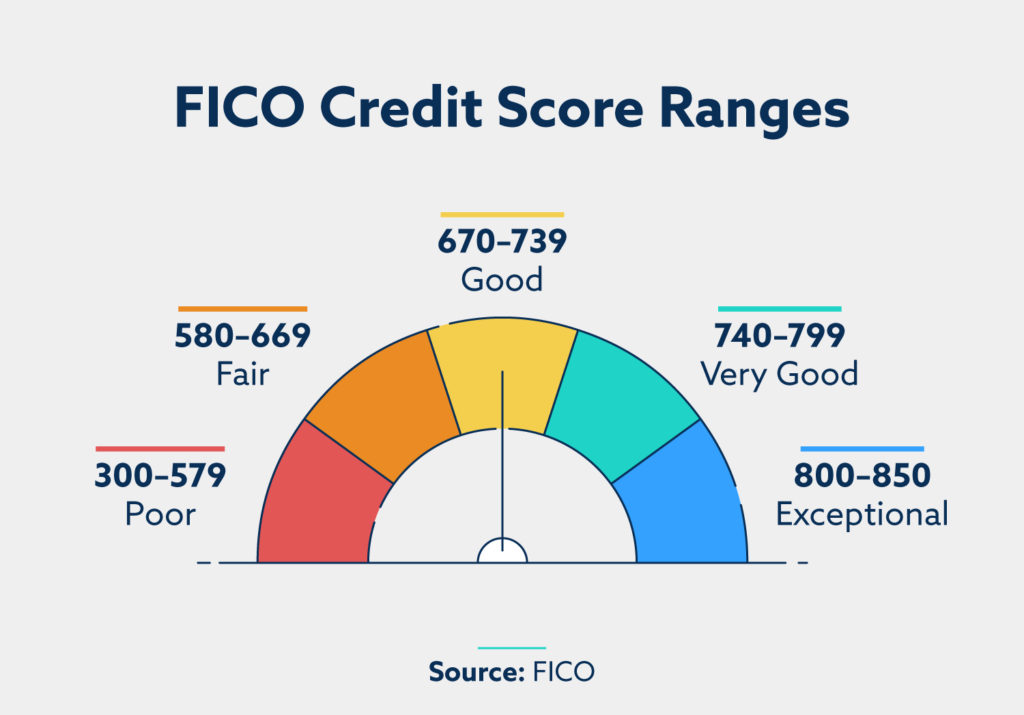

We can keep our credit score good. Good credit gets you lower interest rates. If you have an excellent score of 750 or higher compared to the national average of 717 (Business Insider) you will save 0.30% annually on a 30 year mortgage. On an $800k loan that’s almost $200 per month.

You can start saving early. There’s an old book called “The Richest Man in Babylon.” One of the rules it preaches is to save 10% of what you earn. Here’s the scenario, you make $50k per year starting at age 25 and it increases by 3% each year. If you save 10% of your salary each year and get an 8% rate of return you will accumulate almost $1million by the time you are 57. Wait 5 years to start saving 10% and you have to wait until you are age 60. If you wait until age 40 to start saving you won’t hit that mark until you are almost age 67.

Looking at it a different way using the same scenario, at age 60 your savings would look like this:

| Age to start saving | 25 | 30 | 40 |

| Value at age 60 | $1,292,920 | $1,012,592 | $515,608.3 |

Saving early allows you to potentially retire early. I’ve harped on the importance of saving before so I won’t beat a dead horse.

Get an education. According to the BLS is 2023 a person with a Bachelors degree earned nearly $1500 per week compared to $900 per week for a high school graduate. According to Ziprecruiter the average trade school graduate earns $1230 per week. We can’t rest on our high school diploma laurels anymore. Investing in yourself is one of the best things you can do. I’ll add as an aside, make sure the education you are getting gives you transferrable skills. A bachelors in accounting or computer science is likely to offer more transferrable skills to get you further than a general studies degree. The renowned saxophone player Kenny G famously got a degree in Accounting just in case his music career didn’t work out.

Finally, something you can do to get yourself a better draw is to network. Expand your circle. You might need advice on something some day, a referral to professional services, or maybe you need a new job. Maybe you just need someone to blow off some steam with after work. Your network is the number one place to start. That can be in person or, arguably, even your social media friends. You never know where a connection will take you. It could be a pleasant exchange while waiting for a table at a restaurant, or it could be bigger like learning about a new job opening before it’s posted.

Obviously there are a ton of things you can do to better yourself or create a better drawing hand. This post isn’t meant to be an exhaustive list, just some of the main things I’ve picked up through life. I wish I had focused more on saving earlier on, taken my education more seriously, and continued to expand my network at a younger age. The school of hard knocks and a lemon of a car taught me really quick how fragile our financial lives can become.

Anyone who has other nuggets of wisdom, please reach out to share them! And, if you have financial topics you’d like me to address I’ve love to hear those too.