Back in 1997 when I started in this business there was a new technology called the internet that allowed people to trade stocks, bonds and mutual funds from their living room. At that time the pundits were saying that it would be the end of the financial advisor and the brokerage firm in general. About 10 years ago Roboadvisors made the same threat: cheap portfolios “automatically managed” for you. Now AI is the threat: ask it to build a portfolio for you and do it yourself. Even with all these industry threats, I’m still around along with hundreds of thousands of other advisors and not too worried. Here’s why: humans always will find a way to shoot themselves in the foot. People jump into things without fully understanding them. With AI, unless the user asks specific questions about investments and diversification, chances are you end up in something like the S&P 500 and think you’re fine.

I read countless financial articles every day, and sometimes I jump to the comments section at the end. More often than not there are multiple people saying something to the effect of “just put half your money in SPY (S&P 500) and half in QQQ (NASDAQ 100) and let it sit there.” Over the past 15 years that’s been sage advice. The S&P 500 is heavily weighted toward large US tech companies. We’re in the midst of a big-tech revolution which has provided superior returns. Of course the internet troll’s advice works! But that’s only great advice with hindsight.

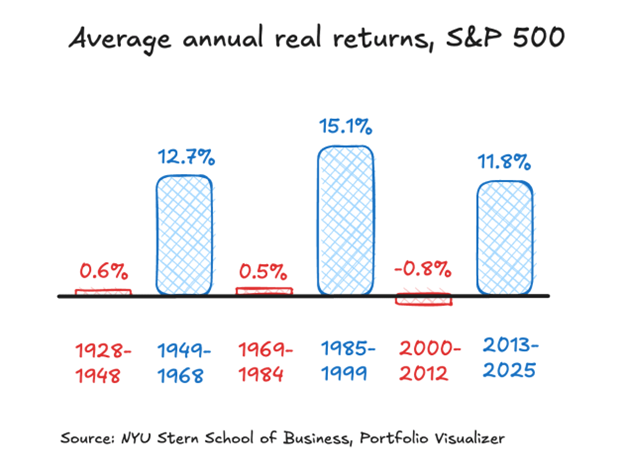

What happens when big tech doesn’t provide superior returns? For a generation of investors and advisors the S&P underperforming seems impossible. That’s not true, and you don’t have to look that far back to see it. Look at the returns of the S&P 500 from NYU Stern School of Business. I clipped this image on Feb 21st from Marketwatch.com “Why you shouldn’t fall in love with the S&P 500”

2000-2010 is often referred to as the lost decade. After the crashes in 2001 and 2008 investors got a rude wakeup call. Advisors started preaching diversification. Anybody remember BRIC (Brazil, Russia, India, China) from those days? That was the new hot asset class and investors couldn’t get enough. Obviously the S&P 500 is back in vogue now. I’ll ask you the question, are you prepared for when it isn’t? History says there will be a turning point, another lost decade, but we never know when.

Let’s say you invest like my standard troll on the internet, 50% to SPY and 50% to QQQ. Those two share 8 of the top 10 and 16 of the top 20 holdings. 50% of the weighting of QQQ is in its top 10 holdings and SPY has 37% in the same holdings. Let’s say you added the S&P Value Index (SPYV) and S&P Growth Index (SPYG). SPYG is going to be almost the same as QQQ and has almost same top 10 holdings as SPY but with different weightings. Wal Mart made the top 10 in QQQ, barely edging out Broadcom. SPYV should be totally different, right? It isn’t. 3 of the top 10 holdings in SPYV are in the top 10 of SPY. These 3 account for 12% of the holdings of SPYV. Curiously, there are 5 companies that are in both the growth and value index: Apple, Amazon, Tesla, JP Morgan and Costco. Riddle me this, how can 5 companies overlap in growth and value according to the same company, Standard and Poors? (Even Chat GPT can’t answer this for me!) The bottom line is these 5 companies make up 14.5% each of the Growth and Value Index.

Regardless of how they calculate what’s in these indexes, the fact of the matter is that if you have a portfolio that is 25% invested in each of the 4 aforementioned ETFs, you have 46% of your assets in the top 20 stocks of QQQ and 39% in the Top 10 of the S&P 500. This isn’t actual diversification. It’s actually very similar to the S&P 500 itself. This matters because investors are not prepared for when large US Tech doesn’t do well. What makes it worse is that they don’t even know they aren’t prepared.

A half good advisor will spot this concentration in a portfolio. In this case at least you would know the risks. More likely you might make some slight changes to actually diversify. One of my standard duties is to review allocations in client 401k accounts. Often times it’ll look very similar to my example portfolio: Tech fund, growth fund, growth and value fund, and index fund. Look at your 401k investment classifications, does this sound familiar?

Actual diversification will include foreign companies, bonds, commodities, and maybe real estate. Hopefully some of these asset classes zig when the S&P 500 zags. You can take advantage of these price discrepancies by rebalancing regularly. Global diversification and regular rebalancing are the core of my investment approach. A wise old-timer from one of the major Wall Street firms once told me, “If you don’t rebalance your portfolio, the market will do it for you.” (i.e. a market correction or crash). Even if you buy a truly diversified portfolio and never rebalance it, chances are that one of the asset classes will run-up to a higher percentage of your holdings than planned. When that asset class corrects, you take higher than expected losses.

Don’t wait until the markets are in turmoil to review things. It’s likely too late by that point. We want to have foresight into something that is virtually impossible to predict. A good advisor will have this foresight. May 401k plans offer in-plan guidance. Use these resources. These could be good starting points. For more in depth analysis, come see me. AI can do a lot, but it is only as good as the questions you ask it. Guys like me can make sure you are asking the right questions.